What Is a Home Equity Loan? A Simple Guide for Homeowners

If you own a home and have paid down your mortgage, you likely have something valuable you may not be fully utilizing: home equity. Whether you’re planning a major home renovation, consolidating debt, or facing an unexpected expense, a home equity loan can be a powerful financial tool.

At Sound Credit Union, serving homeowners across Washington, home equity loans are designed to help you put the equity in your home to work (or play) for you.

This guide explains what a home equity loan is, how it works, what sets it apart from other borrowing options, and what you need to qualify. Whether you’re a first-time home equity borrower or looking to refinance, this guide will help you make an informed decision with confidence.

What Is a Home Equity Loan?

A home equity loan is a type of loan that allows you to borrow money using the equity you’ve built up in your home as collateral. Simply put, home equity is the difference between what your home is currently worth and what you still owe on your mortgage.

For example, if your home is worth $400,000 and you owe $250,000 on your mortgage, you have $150,000 in equity. A home equity loan lets you borrow against that equity, often at a lower interest rate than personal loans, student loans, or credit cards, to fund major expenses or financial goals. They are recommended to be used for ongoing, long-term expenses like medical bills, home renovations, or college tuition.

How Home Equity Loans Work

Home equity loans function differently than personal loans. Here’s the basic process:

- You Apply: You contact your credit union or lender and express interest in borrowing against your home equity. They’ll review your financial situation, credit score, and the current value of your home.

- Apply for a Sound Credit Union home equity loan online.

- The Lender Evaluates Your Equity: The lender determines how much equity you have available to borrow. Most lenders allow you to borrow up to 80-90% of your total home equity, though this can vary.

- You Receive Funds: Once approved, you receive a lump sum of money, either as a direct deposit or a check. You can also access funds via online balance transfer or an Equity credit card for flexibility.

- You Repay Over Time: Like a traditional loan, you repay the borrowed amount plus interest over a fixed period. Typically, this ranges from 5 to 15 years. Your monthly payment remains the same throughout the loan term.

This predictable payment structure makes home equity loans ideal for budgeting and planning.

What Is Home Equity?

Before diving deeper into home equity loans, it’s important to understand what home equity actually is.

Home equity is the portion of your home that you truly own. As you make monthly mortgage payments, you build equity by paying down your principal balance. Additionally, if your home’s value increases due to market appreciation or improvements you’ve made, your equity grows as well.

How to Calculate Your Home Equity

Calculating your home equity is straightforward:

- Home Equity = Current Home Value – Outstanding Mortgage Balance

For example:

- Your home’s current market value: $350,000

- Your remaining mortgage balance: $200,000

- Your home equity: $150,000

This $150,000 represents the equity you’ve built and could potentially borrow against.

Common Uses for Home Equity Loans

Home equity loans can be used for virtually any purpose, but some of the most common include:

- Home Improvements and Renovations: Kitchen remodels, bathroom upgrades, roof repairs, and additions typically increase your home’s value while improving your quality of life.

- Sound also offers Green Fixed Home Equity Loans for energy-efficient home improvements.

- Debt Consolidation: Using a home equity loan to pay off credit cards, personal loans, or other high-interest debt can lower your overall interest rate and simplify your finances.

- Education Expenses: Funding college tuition, vocational training, or other educational costs for yourself or your children.

- Medical Expenses: Covering unexpected medical bills or elective procedures not covered by insurance.

- Home Maintenance: Addressing major repairs like HVAC replacement, foundation work, or plumbing updates.

- Major Life Events: Funding a wedding, adoption costs, or other significant life expenses.

How Much Equity Do I Have in My House?

Wondering how much equity you actually have? There are several ways to find out.

Check Your Mortgage Statements

Your mortgage servicer sends you regular statements that include your current loan balance. Subtract this from your estimated home value to calculate your equity.

Get a Professional Home Appraisal

For a more accurate valuation, consider getting a professional appraisal. This gives you an official assessment of your home’s current market value. When you apply for a home equity loan with Sound, an appraisal is part of the process.

Use Online Home Valuation Tools

Websites like Zillow, Redfin, and Realtor.com provide estimated home values based on recent comparable sales in your area. While not as precise as a professional appraisal, these tools give you a reasonable starting point.

Contact Your Lender

Your credit union or bank can help you determine your home’s equity based on recent appraisals and your current loan balance. Our team can walk you through this process and help you understand exactly how much you can borrow. Call us at 800.562.8130 or visit a local branch to get started.

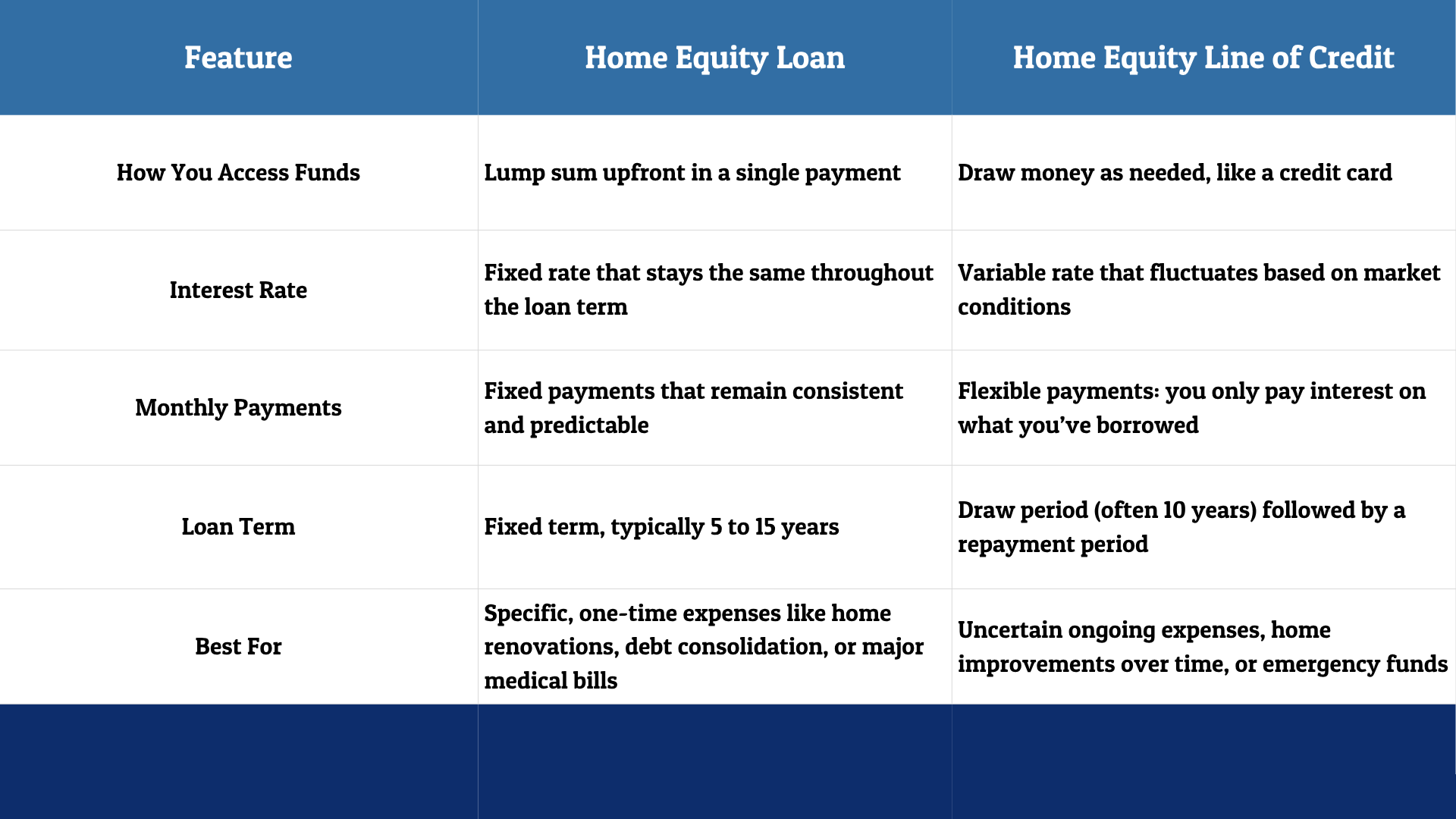

Home Equity Loan vs. HELOC: What’s the Difference?

When exploring ways to borrow against your home equity, you’ll likely encounter two main options: home equity loans and HELOCs (Home Equity Lines of Credit). While both allow you to tap into your home’s equity, they work quite differently.

In short: If you need money now for a specific purpose with predictable payments, a home equity loan is typically the better choice. If you want flexibility and may need to access funds gradually, a HELOC might work better for you. Sound Credit Union offers both options, so you can choose what fits your needs.

Home Equity Loan Requirements, Risks, and Considerations

While requirements vary by lender, most home equity lenders look for the following:

- Credit Score: Most lenders require a credit score of at least 620, though higher scores (680+) typically qualify for better interest rates. Your credit history shows lenders how responsibly you’ve managed debt in the past.

- Home Equity: You’ll need at least 15-20% equity in your home, though most lenders prefer 30% or more. The more equity you have, the more you can potentially borrow.

- Income Verification: Lenders want to ensure you have stable income to make monthly loan payments. You’ll typically need to provide recent pay stubs, tax returns, or W-2s.

- Proof of Homeownership: You must own your home and have a valid mortgage in place. Some lenders may also lend on homes with paid-off mortgages, though terms may vary.

- Current Mortgage Status: You should be current on your mortgage payments with no recent defaults or late payments. A solid payment history demonstrates responsibility.

Home Equity Loan Risks and Considerations

While home equity loans offer many benefits, it’s important to understand the risks:

- Your Home Is Collateral: Unlike unsecured loans, a home equity loan puts your home at risk. If you’re unable to repay the loan, the lender could potentially foreclose on your home. This is why it’s crucial to only borrow what you can comfortably repay.

- Fixed Payments: Once you sign the loan agreement, your monthly payments are set. This predictability is helpful for budgeting, but it also means you’re committed to a specific payment schedule.

- Interest and Principal: Like any loan, you’ll pay interest on the borrowed amount. The interest rate and loan term determine your total cost.

- Closing Costs: Home equity loans typically include closing costs such as appraisal, origination fees, and title search. These can range from 2-5% of the loan amount.

How to Get a Home Equity Loan With Sound Credit Union

Ready to apply for a home equity loan? The process is straightforward and simple.

Step 1: Determine How Much You Can Borrow

Before applying, calculate your available equity and decide how much you need to borrow. Most lenders allow you to borrow 80-90% of your total equity, but not all of it. Remember to leave some equity cushion in your home.

Step 2: Apply for Your Loan

Apply online, call 800.562.8130, or visit a Sound branch to submit your application. Sound makes the process quick and easy, and you’ll find out what rate you qualify for.

Step 3: Submit Documents and Get an Appraisal

To process the loan, Sound will need proof of income and property details. We’ll also send an appraiser out to your home to confirm the current value. This typically takes a few days.

Step 4: Get Your Funds

Once approved, you can access your funds from your Sound account, via online balance transfer, or with an Equity credit card. Funds are typically available within a few days of approval.

Why Choose a Home Equity Loan from Sound Credit Union

Home equity loans from Sound Credit Union often come with distinct advantages compared to traditional banks.

- Lower Interest Rates: As a not-for-profit organization, Sound typically offers more competitive rates. Over the life of your loan, this can save you thousands of dollars.

- Lower Fees: Sound generally charges fewer and lower origination fees, appraisal fees, and closing costs compared to big banks. This means more of your money goes toward paying down your debt.

- Flexible Options: Sound offers multiple ways to access your funds. You can get one lump sum or borrow what you need as you need it. Choose from a fixed home equity loan, an Express Mortgage, a Green fixed home equity loan, or a home equity line of credit.

- Flexible Terms: With terms up to 15 years, Sound provides flexibility in loan terms and may be willing to work with borrowers who have unique financial situations.

- Potential Tax Savings: Interest paid on your home equity loan may be tax-deductible. Check with your tax professional to see if you qualify.

- Easy Access to Funds: Access your line of credit with your Equity credit card or an online balance transfer. Sound makes it convenient to use your funds when you need them.

- Personalized Service: Rather than navigating an automated system, you’ll work with local loan officers who understand your unique situation and can offer guidance tailored to your needs.

- Community Impact: When you borrow from Sound Credit Union, you’re supporting a local financial institution that reinvests profits back into the community you live in.

Ready to Explore Home Equity Loan Options With Sound Credit Union?

If you’re a homeowner in Washington looking to tap into your home’s equity for a major expense or financial goal, Sound Credit Union is here to help. Our home equity loans are designed with your financial well-being in mind, offering competitive rates, transparent terms, flexible options, and personalized guidance every step of the way.

Apply online to get started in a few quick steps, visit a local branch to speak with a loan officer, or call us at 800.562.8130 to learn more about home equity loans.

Tammie Atoigue is the Vice President of Consumer Lending at Sound Credit Union, where she utilizes her extensive experience to empower members in achieving their financial goals. She is passionate about member education, particularly around credit and smart borrowing, and frequently participates in industry speaking engagements to share her insights.

You may also like…

Understanding Trump Accounts: A New Way to Save for Your Child’s Future

A Trump Account is a new type of investment account created for children under age 18, intended to help families build long-term savings and provide young people with a financial foundation as they grow into adulthood.

Business Credit Cards: How They Work and When Your Business Needs One

Learn How Business Credit Cards Work, When Your Company Needs One, and How to Choose the Right Card.

How Do Credit Cards Work: Interest, Limits, and Payments Explained

Learn How Credit Cards Work, Including Interest Rates, Credit Limits, and Payment Terms. Understand APR, Minimum Payments, and How to Use Credit Cards Responsibly to Build Your Financial Future.