Business Credit Cards: How They Work and When Your Business Needs One

If you’re running a business in Washington, whether it’s a startup, a side hustle, or an established company, managing expenses efficiently is important to your success. A business credit card helps you separate personal and business finances, track spending, build credit, and earn rewards on everyday purchases.

At Sound Credit Union, business credit cards are designed to support companies of all sizes with competitive rates, no annual fees, and features that make financial management easier.

This guide explains what business credit cards are, how they work, when your company needs one, and how to choose the right card for your unique business needs.

What Is a Business Credit Card?

A business credit card is a credit card specifically designed for business expenses. Like a personal credit card, it allows you to make purchases on credit up to a certain limit, which you then repay over time. However, business credit cards come with features tailored to the unique needs of companies, such as:

Key Features of Business Credit Cards

- Higher credit limits than personal cards

- Detailed expense management tools and QuickBooks integration

- Unlimited employee cards with individual spending limits

- Rewards on business purchases (office supplies, travel, fuel)

- Purchase protections, including extended warranty and rental car coverage

Ultimately, business credit cards help you keep business expenses separate from personal spending, which simplifies accounting, makes tax preparation easier, and protects your personal credit. When used responsibly, they can also help you build business credit, which is essential for securing loans, lines of credit, and better financing terms in the future.

How Do Business Credit Cards Work?

Business credit cards function similarly to personal credit cards but are designed with business needs in mind. Here’s how they typically work:

- Step One – Apply: You submit an application to your credit union or bank, providing information about your business. The lender will review both your personal and business credit history.

- Apply for a Sound Credit Union business credit card online.

- Step Two – Receive a Credit Limit: Once approved, you’re assigned a credit limit based on factors like your creditworthiness, business revenue, and financial history. Business credit cards typically offer higher limits than personal cards to accommodate business-scale spending.

- Step Three – Use Your Card: Use your business credit card for business-related expenses such as office supplies, travel, inventory, software subscriptions, utilities, and more. Each purchase reduces your available credit until you make a payment.

- Step Four – Receive Your Statement: At the end of each billing cycle, you receive a statement showing all purchases, the total balance owed, the minimum payment due, and the payment due date.

- Step Five – Pay Your Balance: If you pay your full statement balance by the due date, you typically won’t pay any interest. If you carry a balance past the grace period, you’ll pay interest based on your card’s A`nnual Percentage Rate (APR). The more you pay each month, the less interest you’ll owe over time.

- Step Six – Receive Rewards: Many business credit cards offer rewards programs that let you earn cash back, points, or miles on your purchases. These rewards can be redeemed for statement credits, travel, gift cards, merchandise, or deposited directly into your account.

Business Credit Card Requirements

Most business credit card issuers look for:

- Personal Credit Score: Typically 680 or higher, though some cards approve mid-600s. Higher scores qualify for better rates.

- Business Information:

- Legal name and DBA (if applicable)

- Business structure (sole proprietorship, LLC, corporation)

- Employer Identification Number (EIN) or Social Security Number

- Annual revenue and number of employees

- Length of time in business

- Personal Guarantee: Most cards require you to be personally responsible for the debt, meaning late payments can impact your personal credit.

- Income Verification: Business bank statements, tax returns, profit and loss statements demonstrating repayment ability.

Types of Business Credit Cards

Understanding the different types of business credit cards will help you choose the right card for your company. Let’s get into it.

Business Rewards Credit Cards

These cards let you earn rewards on every purchase, typically in the form of cash back, points, or miles.

- Best For: Businesses that make frequent purchases, pay their balance in full monthly, and want to maximize the value of their spending.

- Example: Sound’s Business Rewards Card earns Sound Rewards on every purchase, which can be redeemed for travel, merchandise, gift cards, or cash.

Low-Rate Business Credit Cards

These cards offer lower interest rates compared to rewards cards, making them a better choice if you occasionally need to carry a balance. While they may not offer robust rewards programs, the lower APR can save you money on interest charges.

- Best For: Businesses that may need to carry a balance from time to time or are focused on minimizing interest costs.

- Example: Sound’s Business Platinum Card offers competitive rates starting as low as 10.45% APR with no annual fee.

Secured Business Credit Cards

Secured business credit cards require you to provide collateral (typically a cash deposit in a savings account) that serves as security for the credit line. These cards are ideal for new businesses or business owners with limited or poor credit history.

- Best For: New businesses, startups, or business owners building or rebuilding credit.

- Example: Sound’s Business Platinum Secured Card helps you establish business credit while enjoying purchase protection and competitive rates.

Charge Cards

Unlike traditional credit cards, charge cards require you to pay your balance in full each month. They typically don’t have a preset spending limit, making them useful for businesses with large, predictable expenses that can be paid off quickly.

- Best For: Established businesses with consistent cash flow and the ability to pay balances in full monthly.

How to Choose the Right Business Credit Card

Step 1: Determine Your Primary Goal

- Earning Rewards: Choose a business rewards card if you pay in full monthly

- Minimizing Interest: Select a low-rate card if you carry balances

- Building Credit: Consider a secured card for new businesses

- Managing Employees: Look for unlimited authorized signers

Step 2: Analyze Your Spending Patterns

Review recent expenses to identify:

- Monthly spending amount

- Top spending categories (travel, office supplies, fuel)

- Whether you pay in full or carry balances

Step 3: Compare Card Features

- Interest Rate (APR): Lower APRs save money when you carry a balance from month to month.

- Annual Fees: Many business cards charge $0 annual fees, helping you avoid unnecessary costs.

- Foreign Transaction Fees: If your business operates internationally, cards without these fees save you 1-3% on every overseas purchase.

- Sign-Up Bonuses: New cardholders often qualify for one-time bonuses like cash back or bonus points after meeting spending minimums.

- Rewards Program: Choose a program that matches your actual spending (travel, dining, office supplies) to maximize value.

- Employee Card Policies: Set spending limits and controls for team cards to manage business expenses and prevent overspending.

- Expense Management Tools: Built-in software integration and analytics help you track spending, categorize expenses, and simplify accounting.

- Purchase Protections: Extended warranties, fraud protection, and purchase guarantees provide peace of mind on major business purchases.

Step 4: Read the Fine Print

Review terms and conditions, fee schedules, reward earning and redemption rules, and grace period length.

Step 5: Apply

Apply for a business credit card online, over the phone, or in person.

When Your Business Needs a Credit Card

Not every business needs a credit card right away, but there are several situations where having one makes sense. Here are common scenarios where a business credit card can be beneficial:

You Have Employees Making Purchases

If your team regularly makes business purchases (travel, office supplies, etc.), employee cards simplify expense management by:

- Consolidating all charges on one monthly statement

- Eliminating manual expense reports and reimbursement delays

- Giving you real-time visibility into company spending

At Sound Credit Union, we offer unlimited authorized signers at no extra cost, making it easy to equip your entire team.

You Want to Build Business Credit

Building a strong business credit profile is important for securing loans, lines of credit, and favorable financing terms in the future. Using a business credit card responsibly by making on-time payments and keeping your balance low helps establish and improve your business credit score.

Make sure your card issuer reports to commercial credit bureaus like Dun & Bradstreet, Experian Business, and Equifax Business to build your profile.

You Want to Earn Rewards on Business Spending

If your business has regular, predictable expenses (office supplies, travel, fuel, software subscriptions, advertising), a business rewards credit card can help you earn cash back or points on purchases you’re already making. Over time, these rewards can add up significantly, providing valuable savings or perks that benefit your business.

Benefits of Using a Business Credit Card

Using a business credit card responsibly offers numerous advantages for business owners:

1. Separate Business and Personal Finances

Keeping business expenses separate from personal spending helps with:

- Simplified Tax Preparation: When business expenses are clearly separated, tracking deductions becomes much easier, saving time and reducing stress during tax season.

- Accurate Financial Reporting: Clean separation helps you prepare accurate profit and loss statements, balance sheets, and cash flow reports.

- Reduced Audit Risk: Mixing personal and business expenses can raise red flags with the IRS. A dedicated business card helps ensure you’re only claiming legitimate business deductions.

- Legal Protection: For incorporated businesses (LLCs, corporations), maintaining separate finances helps preserve the legal separation between you and your business, protecting your personal assets.

2. Improve Cash Flow Management

Business credit cards offer a grace period (typically 21-30 days) during which you can make purchases without paying interest, as long as you pay the full balance by the due date. This flexibility can help you manage cash flow by allowing you to:

- Pay vendors and suppliers upfront while waiting for customer payments

- Cover unexpected expenses without depleting cash reserves

- Take advantage of early payment discounts from suppliers

- Smooth out seasonal fluctuations in revenue

3. Simplify Expense Tracking and Accounting

Business credit cards make it easier to track and categorize your spending. Most cards provide:

- Detailed Monthly Statements: Itemized lists of all purchases with merchant names, dates, and amounts

- Spending Reports: Many cards automatically categorize expenses (travel, office supplies, dining) to simplify bookkeeping

- Software Integration: Direct integration with accounting software like QuickBooks, allowing you to import transactions automatically and streamline your monthly close.

4. Access Purchase Protections and Benefits

Many business credit cards include valuable protections and benefits such as:

- Purchase Security: Protection against damage or theft of items purchased with your card

- Extended Warranty: Extends manufacturer warranties on eligible purchases

- Auto Rental Collision Damage Waiver: Coverage when you rent vehicles for business purposes

- Travel and Emergency Assistance: Help with travel-related issues like lost luggage, medical emergencies, or travel disruptions

These benefits provide added value and peace of mind, potentially saving your business money when unexpected issues arise.

Common Mistakes to Avoid With Business Credit Cards

- Mixing Personal and Business Expenses: Even with a business credit card, it’s crucial to only use it for legitimate business expenses. Using your business card for personal purchases defeats the purpose of separation and can create tax and legal issues.

- Carrying High Balances: Just like personal credit cards, carrying high balances on business cards can hurt your credit utilization ratio and increase interest costs. Aim to keep your balance below 30% of your credit limit, and pay in full whenever possible.

- Missing Payments: Late payments can damage both your business and personal credit scores, result in late fees, and increase your interest rate. Set up automatic payments or reminders to ensure you never miss a due date.

- Not Monitoring Employee Cards: If you issue employee cards, regularly review their spending to ensure purchases are appropriate and within budget. Set up alerts to notify you of transactions and establish clear policies about acceptable use.

- Ignoring Rewards and Benefits: If you have a rewards card, make sure you’re actually using the rewards you earn. Points and cash back don’t help your business if they expire unused. Similarly, take advantage of benefits like purchase protection and extended warranties when relevant.

- Applying for Too Many Cards at Once: Each credit card application triggers a hard inquiry on your credit report, which can temporarily lower your credit score. Apply for cards strategically and space out applications to minimize the impact.

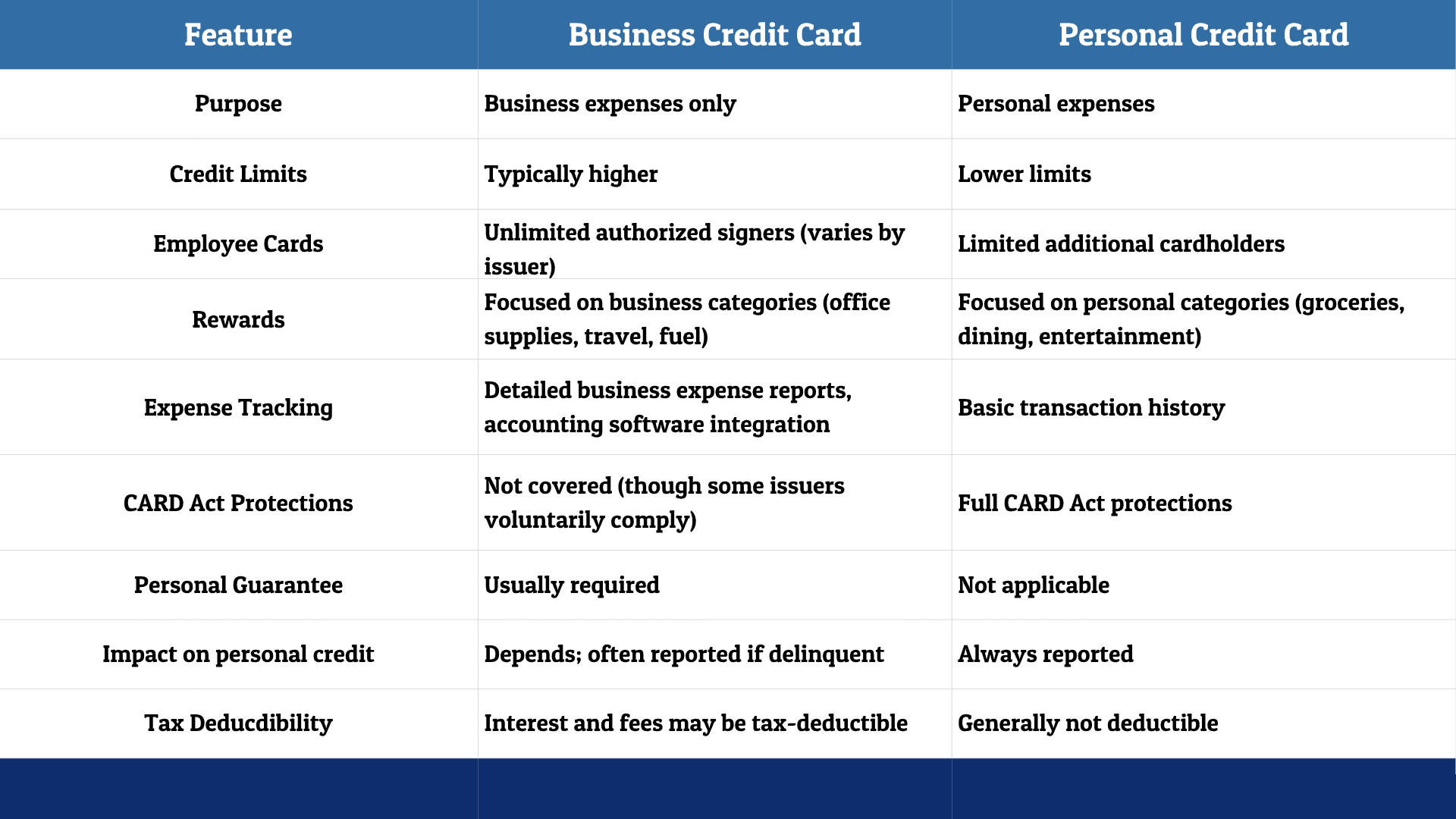

Business Credit Cards vs. Personal Credit Cards: Key Differences

While business and personal credit cards function similarly, there are important differences to understand:

Why Choose a Business Credit Card from Sound Credit Union

Sound Credit Union’s business credit cards offer distinct advantages for Washington business owners:

- No Annual Fees: All Sound business credit cards come with $0 annual fees, helping you keep more money in your business.

- Competitive Rates: As a not-for-profit credit union, Sound offers competitive APRs ranging from 10.45% to 22.45%, depending on the card and your creditworthiness. This often beats rates from traditional banks.

- Unlimited Authorized Signers: Equip your entire team with employee cards at no extra cost. Set individual spending limits and monitor all purchases on one consolidated statement.

- No Foreign Transaction Fees: If your business involves international travel or purchases from foreign vendors, you won’t pay extra fees on those transactions.

- Sound Rewards Program: With the Business Rewards Card, earn points on every purchase that can be redeemed for travel, merchandise, gift cards, or cash, giving you flexibility in how you use your rewards.

- Purchase Protections: All Sound business credit cards include purchase security, extended warranty protection, auto rental collision damage waiver, and travel and emergency assistance services.

- Tech-Savvy Security Features: Protect your business with EMV chip technology, real-time text and email alerts, and card lock/unlock features in Sound’s mobile app.

- QuickBooks Integration: Direct Connect for QuickBooks allows you to download account information directly into your accounting software, streamlining bookkeeping and monthly close processes.

- Fast Approvals: Get approved for your card in minutes online, over the phone, or in a branch, helping you access credit when you need it.

- Local, Personalized Service: Unlike big banks, Sound Credit Union provides local support from a team that understands your business and is invested in your success. You’re building a relationship, not just opening an account.

- Community Impact: When you bank with Sound Credit Union, you’re supporting a local financial institution that reinvests in the Washington communities you live and work in.

Ready to Apply for a Business Credit Card?

If you’re a Washington business owner looking to separate finances, manage cash flow, earn rewards, or build credit, Sound Credit Union’s business credit cards can help.

Compare our business credit card options:

- Business Rewards Card: Earn Sound Rewards on every purchase

- Business Platinum Card: Competitive low rates starting at 10.45% APR

- Business Platinum Secured Card: Build credit with a secured card

Apply online to get started in minutes, visit a local branch to speak with a business banking specialist, or call us at 800.562.8130 to learn more about business credit cards and discover how we can help you achieve your business goals.

Tammie Atoigue is the Vice President of Consumer Lending at Sound Credit Union, where she utilizes her extensive experience to empower members in achieving their financial goals. She is passionate about member education, particularly around credit and smart borrowing, and frequently participates in industry speaking engagements to share her insights.

You may also like…

Understanding Trump Accounts: A New Way to Save for Your Child’s Future

A Trump Account is a new type of investment account created for children under age 18, intended to help families build long-term savings and provide young people with a financial foundation as they grow into adulthood.

What Is a Home Equity Loan? A Simple Guide for Homeowners

Wondering “What Is a Home Equity Loan”? Find All the Answers You’ll Need Here, Including How They Work, Requirements to Qualify, and How to Get One.

How Do Credit Cards Work: Interest, Limits, and Payments Explained

Learn How Credit Cards Work, Including Interest Rates, Credit Limits, and Payment Terms. Understand APR, Minimum Payments, and How to Use Credit Cards Responsibly to Build Your Financial Future.